Life insurance isn’t just something you buy because someone told you to — it’s a financial decision that can affect your family’s security, your long‑term planning, and even your investment strategy. But with so many types of life insurance out there, two options always come up in conversation:

🟢 Term Life Insurance

🟣 Whole Life Insurance

Let’s break it down in a relaxed, conversational way, not like a boring financial lecture.

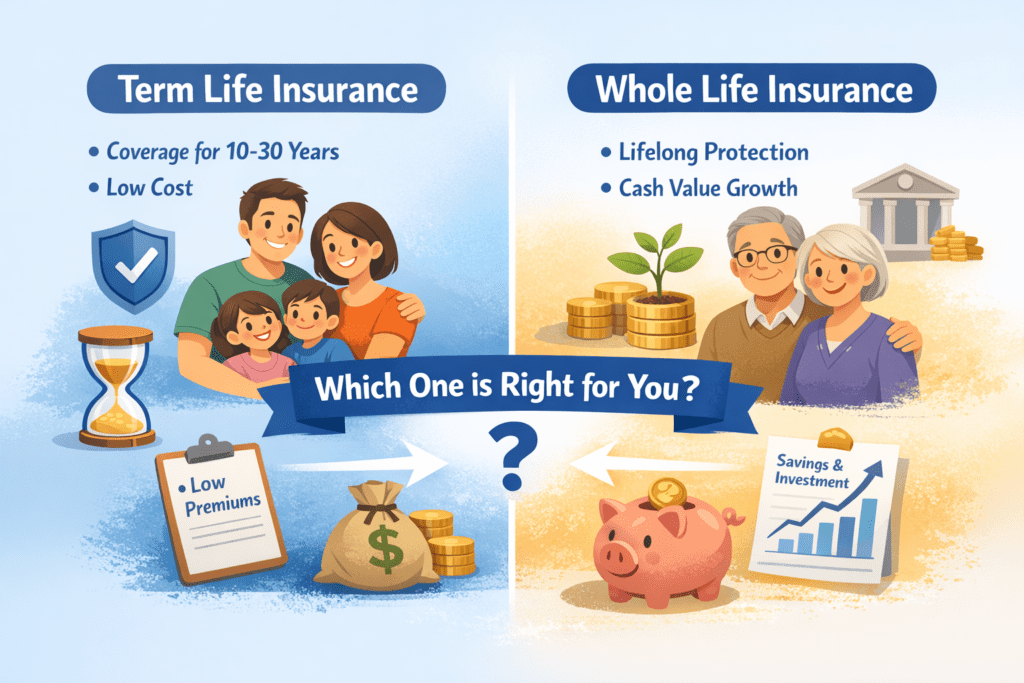

1. Term Life Insurance — Simplicity & Affordability

Imagine this: you want life coverage only during the years your family depends on your income — like when the kids are young or when you have a mortgage.

📌 Term life insurance does exactly that.

- Coverage for a fixed period — e.g., 10, 20, or 30 years

- Lower premiums compared to permanent policies

- Straightforward protection — no investment inside

👉 The main advantage?

💸 It’s affordable. You get strong protection without paying a lot.

👉 The catch?

❗If your term ends and you’re still breathing, there’s no payout or cash value.

This makes term life insurance something like paying for a safety net that disappears if you never need it — but that’s okay, because ideally you don’t need it when you’re older and financially independent.

2. Whole Life Insurance — Protection + Savings All in One

Now picture something that isn’t just a safety net — something that also grows in value over time.

That’s whole life insurance.

✔️ Lifetime coverage — as long as you pay premiums

✔️ Cash value — builds up like a savings account

✔️ Guaranteed death benefit

It’s like buying protection and a forced way to save money.

But here’s the honest part:

Whole life insurance costs more.

A lot more — especially in the early years.

Why?

💡 Because part of your premium goes into a cash value component (think of it as a slowly growing investment) and part goes to the insurance company to guarantee lifetime coverage.

3. Side‑by‑Side: Key Differences

| Feature | Term Life | Whole Life |

|---|---|---|

| Coverage Duration | Fixed term (e.g., 20 yrs) | Lifetime |

| Cash Value | ❌ | ✅ Builds over time |

| Premium Cost | Low | High |

| Best For | Pure protection | Protection + savings/investment |

4. Which One Is Right For You?

Here’s the real talk — there is no one answer that fits everyone. But ask yourself:

🧠 If you want:

- A budget‑friendly policy

- Coverage just while you’re working and supporting dependents

➡️ Term Life is your answer.

💡 If you want:

- Coverage that lasts your entire life

- A guaranteed death benefit plus savings component

- A forced way to grow value over time

➡️ Whole Life might fit you.

5. But What About CASH VALUE?

This part confuses a lot of people — especially those who think insurance isn’t an investment.

Here’s the easiest way to think about it:

🟩 Term Life = Pure protection

🟩 Whole Life = Protection + a slow growing financial bucket

However, if your only goal is investment growth, other assets (like stocks, ETFs, real estate) often give higher returns than the cash value of a whole life policy.

So before choosing whole life for investment reasons alone, ask:

👉 “Am I willing to trade higher returns for guaranteed safety?”

If yes, great — whole life could make sense as part of a diversified plan.

If not, you might be better with pure investment accounts + term coverage.

6. Final Thought — No Regrets Planning

The best financial move isn’t the flashiest one — it’s the one you understand and feel confident about.

So take the time to:

✔️ Compare quotes from multiple insurers

✔️ Understand cost vs benefit clearly

✔️ Evaluate your long‑term goals

Life insurance isn’t just a contract — it’s a commitment to the financial future of the people you care about.