When people start looking for a loan, one of the first questions they encounter is whether to choose a secured loan or an unsecured loan. At first glance, both options may seem similar because they both provide access to borrowed money that must be repaid with interest. However, the way these loans work—and the risks involved—are quite different. Understanding the difference between a secured loan vs unsecured loan can help borrowers make smarter financial decisions and avoid unnecessary risks.

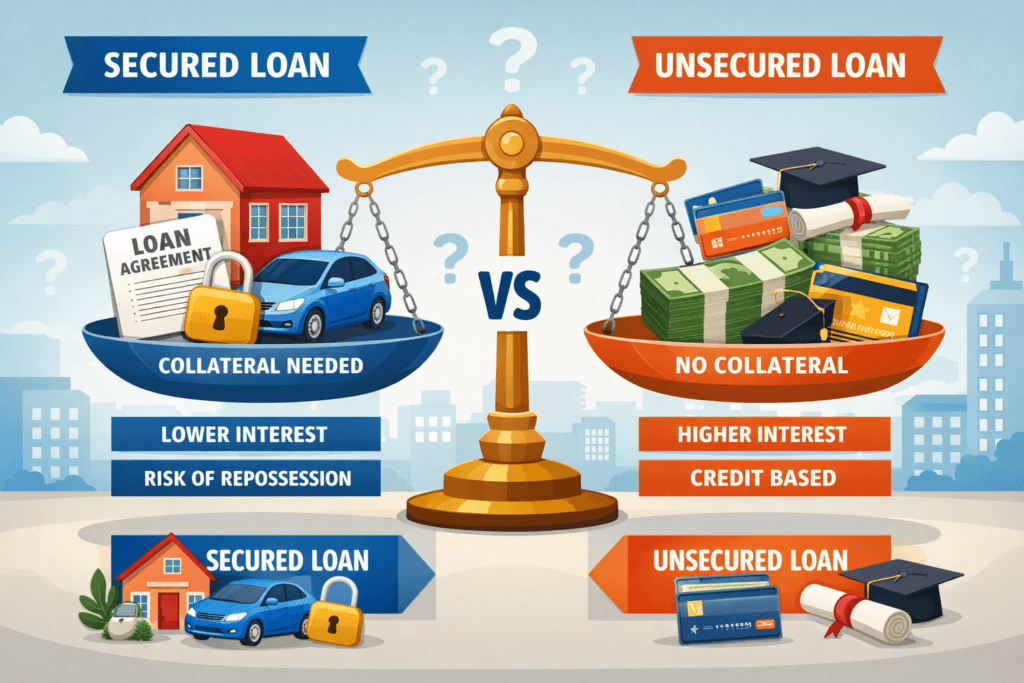

A secured loan is a type of loan that requires collateral. Collateral is an asset the borrower pledges to the lender as security for the loan. Common examples of collateral include a house, a car, savings accounts, or other valuable property. If the borrower fails to repay the loan, the lender has the legal right to take the collateral to recover the money.

Mortgages and auto loans are the most common examples of secured loans. When someone takes out a mortgage, the house itself becomes the collateral. Similarly, when financing a car purchase, the vehicle serves as security for the lender. Because the lender has a form of protection, secured loans usually offer lower interest rates and higher borrowing limits compared to unsecured loans.

For borrowers with strong financial discipline, secured loans can be a cost-effective way to borrow money. Lower interest rates mean smaller monthly payments and less total interest over time. In addition, secured loans may be easier to qualify for, especially for borrowers who have limited credit history or a lower credit score. The collateral reduces the lender’s risk, making approval more likely.

However, secured loans come with a major risk. If the borrower cannot make payments, the lender can seize the asset. Losing a car or home due to loan default can have serious long-term consequences. For that reason, borrowers should carefully evaluate their financial stability before using valuable assets as collateral.

On the other hand, an unsecured loan does not require collateral. Instead, lenders approve these loans based primarily on the borrower’s creditworthiness. Credit score, income, employment stability, and debt-to-income ratio all play important roles in determining eligibility.

Common examples of unsecured loans include personal loans, credit cards, and student loans. Because the lender does not have collateral as protection, these loans typically carry higher interest rates compared to secured loans. Lenders compensate for the increased risk by charging more in interest.

Despite higher interest rates, unsecured loans offer a key advantage: borrowers do not risk losing personal assets if they fail to repay the loan. While missed payments can damage credit scores and lead to collections, lenders cannot immediately seize property as they would with a secured loan.

Another difference between secured loan vs unsecured loan lies in the approval process. Secured loans may require asset evaluation, ownership verification, and additional paperwork related to the collateral. Unsecured loans, especially online personal loans, can sometimes be approved much faster because they rely mostly on credit checks and financial data.

Borrowing limits also tend to differ. Secured loans usually allow borrowers to access larger amounts of money since the lender has collateral as security. Unsecured loans often have lower limits, especially for borrowers with average credit scores.

Choosing between these two types of loans ultimately depends on the borrower’s financial situation and risk tolerance. If someone needs a large loan amount and has valuable assets available as collateral, a secured loan may provide lower interest rates and better repayment terms. However, if protecting personal assets is the priority, an unsecured loan may be the safer choice even with higher interest costs.

Another important factor to consider is long-term financial planning. Borrowers should evaluate how the loan fits into their overall financial strategy. A loan should not only solve a short-term problem but also remain manageable within future income and expenses.

In the end, the debate between secured loan vs unsecured loan is not about which option is universally better. Instead, it is about understanding the trade-offs between risk, interest rates, and borrowing flexibility. By carefully evaluating both options, borrowers can choose the loan type that aligns best with their financial goals and reduces the chances of future financial stress.

Making informed borrowing decisions is one of the most important steps toward building long-term financial stability.