The way people manage money has changed dramatically over the last decade. I still remember when visiting a physical bank branch was unavoidable—standing in long lines just to transfer funds or check balances. Today, everything happens in seconds through a smartphone.

This shift has sparked a big question many readers ask: Is digital banking really safer than traditional banks?

Let’s break it down clearly, without hype, and from a real financial perspective.

What Is Digital Banking?

Digital banking refers to financial services that operate primarily online. These platforms allow users to open accounts, save money, invest, transfer funds, and even apply for loans without visiting a physical branch.

Unlike traditional banks, digital banks rely heavily on financial technology (fintech) infrastructure, automation, and AI-driven risk management.

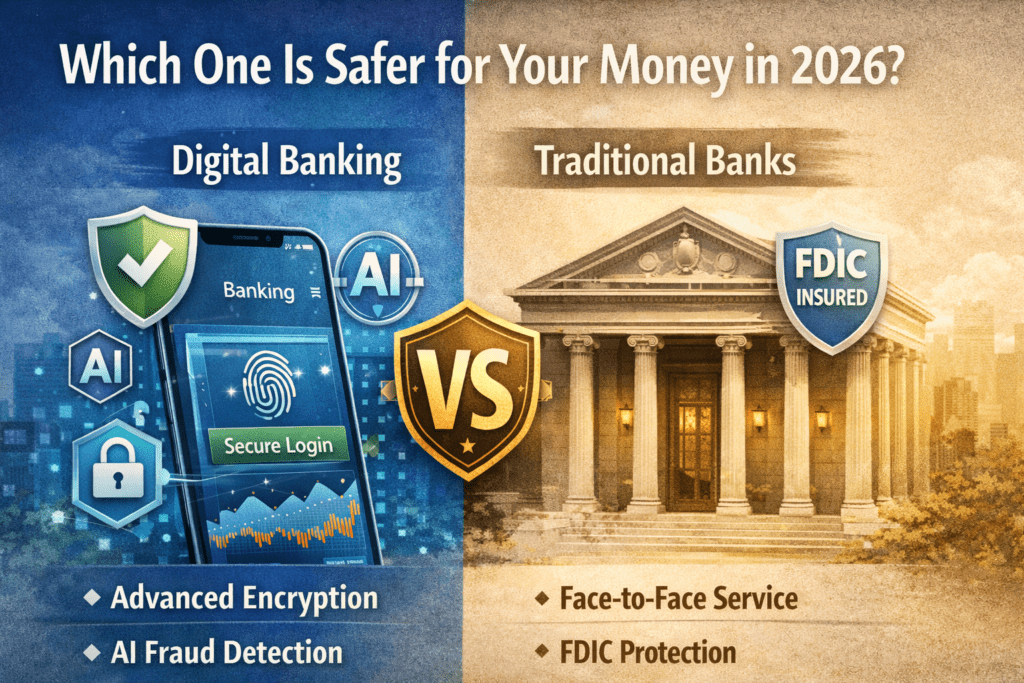

Security Comparison: Digital Banking vs Traditional Banks

1. Data Protection & Encryption

Modern digital banks use advanced encryption standards, multi-factor authentication, and biometric security. In many cases, their cybersecurity systems are more up-to-date than traditional banks that still rely on legacy infrastructure.

Traditional banks, while regulated and insured, often struggle with outdated systems that are harder to upgrade quickly.

Winner: Digital Banking

2. Fraud Detection & AI Monitoring

One of the biggest advantages of fintech platforms is real-time fraud detection. AI algorithms monitor transactions instantly and can freeze suspicious activity within seconds.

Traditional banks usually detect fraud after it happens, relying on manual reviews or delayed alerts.

Winner: Digital Banking

3. Regulatory Compliance & Insurance

Traditional banks have a long history of strict regulation and government-backed insurance. This still gives them an edge in terms of institutional trust.

However, many digital banks now operate under the same regulatory frameworks and offer insured accounts, especially in major financial markets.

Winner: Traditional Banks (slight edge)

Cost Efficiency: Why Digital Banks Are More Profitable for Users

Digital banks eliminate physical branches, reducing operational costs. These savings are passed on to users through:

- Lower transaction fees

- Higher savings interest rates

- Better foreign exchange rates

From my experience, these cost advantages are one of the biggest reasons users switch to fintech platforms.

User Experience & Accessibility

Digital banking platforms are designed with simplicity in mind. Account setup often takes less than 10 minutes, and customer support is available 24/7 through chat systems.

Traditional banks still rely heavily on office hours and in-person verification, which can slow everything down.

Winner: Digital Banking

Risks You Should Still Be Aware Of

No system is perfect. Digital banking does come with risks such as:

- Dependence on internet access

- Platform-specific outages

- Less human interaction for complex cases

That’s why smart users often combine both digital and traditional banking services.

Final Verdict: Which One Should You Choose?

If you value speed, lower fees, advanced security, and convenience, digital banking is clearly the future.

If you prefer face-to-face support and long-established institutions, traditional banks still have their place.

The smartest financial strategy in 2026 is not choosing one—but using both wisely.

Frequently Asked Questions (SEO Boost)

Is digital banking safe for large amounts of money?

Yes, as long as the platform is regulated and uses modern security protocols.

Can digital banks replace traditional banks completely?

Not yet. They complement each other rather than compete directly.

Why are fintech platforms growing so fast?

Lower costs, better user experience, and technology-driven efficiency.