out your first personal loan can be intimidating. There are so many options—from traditional banks to online fintech platforms—that it’s easy for beginners to feel lost. But understanding the basics and comparing offers carefully can help you find the best personal loans for your needs.

Personal loans can be a helpful tool for covering unexpected expenses, consolidating debts, or financing life events like education or home improvements. However, to make the most of a loan, beginners should learn how to evaluate interest rates, fees, repayment schedules, and their own financial capacity.

Why Personal Loans Matter for Beginners

Personal loans are versatile. They allow borrowing for a variety of purposes:

- Consolidating multiple debts into a single monthly payment.

- Paying for medical expenses or emergencies.

- Funding home renovations, travel, or small business ventures.

Unlike credit cards, personal loans usually come with fixed interest rates and set repayment schedules, which can help beginners budget effectively.

💡 Tip: Always match the loan purpose with your repayment ability. Overborrowing is a common mistake that can lead to financial stress.

How to Choose the Right Personal Loan

When searching for the best personal loans for beginners, consider these key factors:

1. Interest Rates:

Lower rates mean you pay less over the life of the loan. Compare different lenders, including online platforms, to find competitive rates.

2. Repayment Terms:

Shorter terms can reduce interest payments but increase monthly obligations. Longer terms may feel easier monthly but cost more in total interest.

3. Fees and Penalties:

Watch out for hidden fees, early repayment penalties, or processing costs. Some lenders advertise low rates but include fees that raise the overall cost.

4. Loan Amount Flexibility:

Ensure the lender offers amounts suitable for your needs without overextending your finances.

5. Application Process and Speed:

Fintech platforms often provide faster approvals compared to traditional banks. Decide whether speed or reliability matters more for your situation.

💡 Tip: Use online calculators to estimate monthly payments before committing.

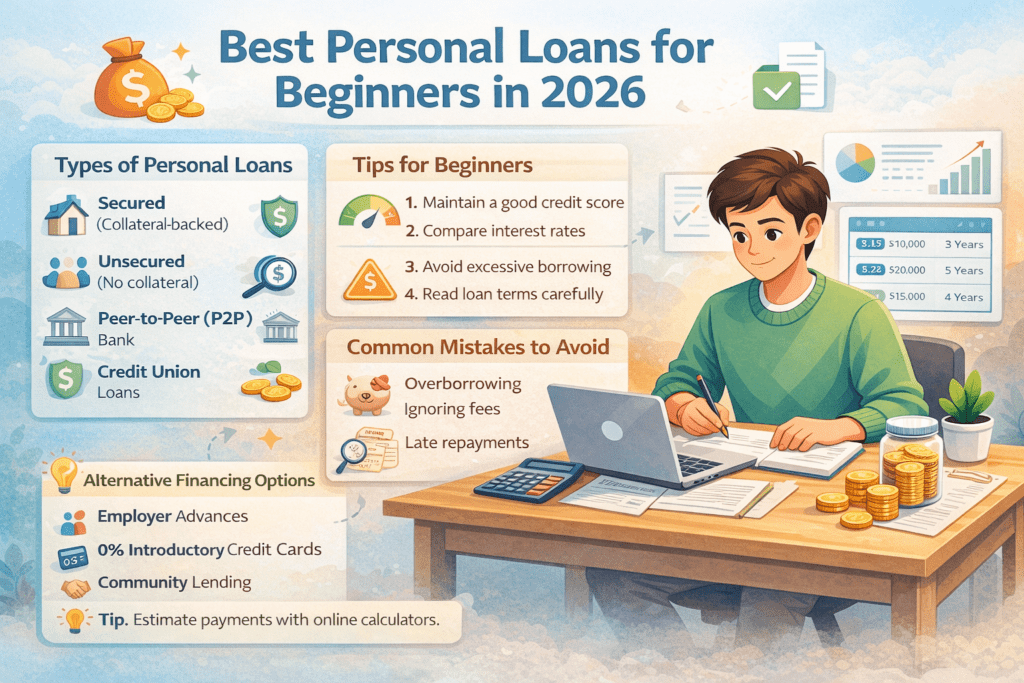

Types of Personal Loans for Beginners

Secured Loans: Require collateral, like a car or savings account. Lower interest rates but risk losing the asset if you default.

Unsecured Loans: No collateral required. Easier to qualify for but usually higher interest rates.

Peer-to-Peer (P2P) Loans: Borrow from individuals via online platforms. Typically faster approval and flexible terms.

Bank Loans: Traditional option with structured processes and customer support. Usually more reliable but slower approval.

Credit Union Loans: Often lower interest and more flexible terms for members.

Each loan type has pros and cons. Beginners should evaluate based on their personal risk tolerance and repayment capacity.

Tips to Improve Loan Approval Chances

- Maintain a good credit score. Lenders use this to gauge reliability.

- Keep your monthly debt-to-income ratio low to increase approval likelihood.

- Provide accurate and complete documentation to avoid delays.

- Avoid applying for multiple loans at once, as this can negatively affect your credit score.

Mistakes Beginners Often Make

- Borrowing more than necessary. Only take what you can repay comfortably.

- Ignoring interest rates and fees. Always read the fine print.

- Missing repayments. Late payments damage credit scores and incur extra charges.

- Relying solely on friends’ advice. Loans and personal finances are unique for everyone.

Dollar-Cost Averaging Concept Applied to Loans

While commonly associated with investments, a similar principle can help with loans: consistent, manageable repayment. Beginners should plan monthly payments that they can sustain, avoiding financial strain.

Alternatives to Traditional Personal Loans

If you’re hesitant to take a loan, consider:

- Employer Advances or Emergency Funds: Some companies provide small interest-free loans for employees.

- 0% Introductory Credit Cards: Can be used for short-term borrowing if repaid promptly.

- Community Lending Programs: Credit unions or non-profits sometimes offer lower-interest loans.

These alternatives may reduce risk and provide better control over finances.

Planning Your Loan Repayment

- Budget Carefully: Allocate funds for your loan before discretionary spending.

- Set Reminders: Automate payments or set calendar alerts to avoid late fees.

- Consider Early Repayment: If finances allow, paying off the loan early reduces interest costs.

💡 Practical Tip: Keep a loan tracker sheet, noting amounts borrowed, monthly payments, and remaining balance. This helps visualize progress and motivates on-time payments.

When to Avoid Taking a Loan

- You lack a stable income to cover monthly repayments.

- The loan has unusually high interest or hidden fees.

- You’re already struggling with multiple debts.

In such cases, consider saving first or exploring alternative financing methods.

Conclusion

Finding the best personal loans for beginners requires careful planning, research, and awareness of your financial situation. Compare interest rates, fees, repayment schedules, and alternatives before making a decision.

With patience and careful selection, personal loans can be a powerful tool for achieving short-term goals or consolidating debt. Begin with a clear repayment plan, stay disciplined, and avoid unnecessary borrowing.

For additional guidance, practical tools, and financial tips, visit Investney.com to confidently manage your loans and grow your financial knowledge.