Banking has changed.

You no longer need to stand in line.

You don’t need paper statements.

You don’t even need a physical branch.

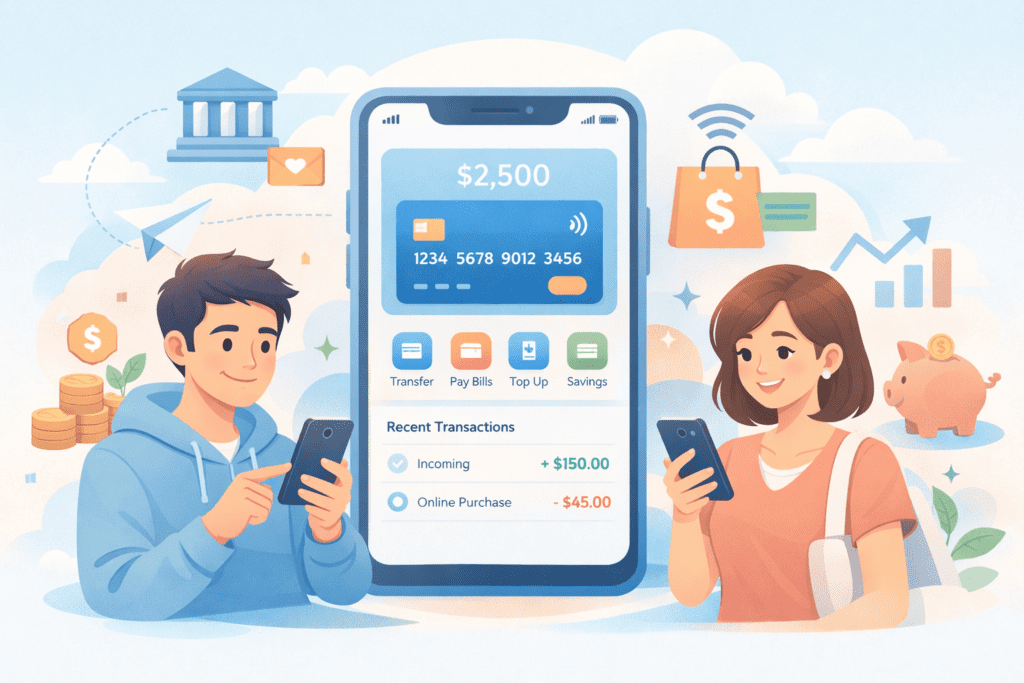

A digital banking app allows you to manage your entire financial life directly from your smartphone.

But convenience is only part of the story.

Let’s break down how it works — and how to use it safely.

What Is a Digital Banking App?

A digital banking app is a mobile application provided by a bank or fintech company that allows users to:

- Open accounts

- Transfer money

- Pay bills

- Track spending

- Save automatically

- Invest (in some cases)

Some digital banks operate without physical branches. These are often called “neobanks.”

The goal?

Faster, simpler, cheaper banking.

How a Digital Banking App Works

When you download the app:

- You create an account

- Verify your identity (KYC process)

- Link funding source

- Start managing money digitally

Behind the scenes, the app connects to banking infrastructure and payment networks securely.

Security features typically include:

- Biometric login

- Two-factor authentication

- Real-time fraud alerts

- Encryption technology

Modern fintech platforms prioritize user experience and security.

Key Features of a Good Digital Banking App

Not all apps are equal.

Here are essential features to look for:

1️⃣ Real-Time Spending Insights

Instant transaction notifications help control spending.

2️⃣ Automated Savings Tools

Round-up features or scheduled transfers make saving effortless.

3️⃣ Low or No Fees

Many fintech banks reduce or eliminate monthly maintenance fees.

4️⃣ Fast Transfers

Instant or same-day transfers improve cash flow flexibility.

5️⃣ Integrated Investing

Some apps allow users to invest in stocks, ETFs, or crypto.

Convenience plus control — that’s the fintech advantage.

Benefits of Using a Digital Banking App

Here’s why adoption is growing globally:

- 24/7 access

- Lower operational costs

- Faster transactions

- Transparent fee structures

- Budget tracking built-in

For younger generations especially, mobile-first finance is standard.

Risks to Consider

Technology is powerful — but not perfect.

Risks include:

- Cybersecurity threats

- App outages

- Hidden fees in premium tiers

- Overdependence on mobile access

That’s why choosing a regulated and reputable provider is essential.

Digital Banks vs Traditional Banks

Traditional banks:

- Physical branches

- Higher overhead costs

- Broader service range

Digital banks:

- Mobile-first

- Lower fees

- Faster onboarding

Many consumers now use both — combining stability with innovation.

How to Choose the Best Digital Banking App

Follow this checklist:

- Check regulatory status

- Read user reviews

- Compare fee structure

- Test app interface

- Evaluate customer support access

Ease of use matters — but security matters more.

Is a Digital Banking App Safe?

Generally, yes — if regulated.

Look for:

- FDIC (US) or equivalent deposit insurance

- Encryption protocols

- Fraud monitoring systems

Security today is often stronger than traditional branch systems — because digital platforms invest heavily in cybersecurity.

The Future of Digital Banking

Fintech is expanding into:

- AI-powered budgeting

- Embedded finance

- Crypto integration

- Instant global payments

- Open banking ecosystems

Digital banking apps are not just replacing branches.

They’re redefining financial management entirely.

Final Thoughts

A digital banking app is more than convenience.

It’s financial empowerment in your pocket.

Used wisely, it helps you:

- Track spending

- Save automatically

- Transfer instantly

- Invest smarter

The future of finance is digital.

The question is not whether fintech will grow.

The question is whether you’re ready to use it strategically.

Hey folks! Looking for info on 7m. ma cao? This is the right corner of the internet, great site! Click here: 7m. ma cao